- Can I Make Unequal Payments?

- What If I Fail to Pay?

🔃Updated January 2024 with figures and dates for 2024 and updated screenshots for the worksheets included in 2024 Form 1040-ES: Estimated Tax for Individuals.

What Are Estimated Tax Payments?

Our tax code requires you to pay taxes as you earn income.

If you’re a W-2 employee, you have tax withheld on every paycheck by your employer. This is based on what you enter on a Form W-4.

At the end of the year, you fill out your tax return, figure out your actual tax liability, and pay the difference or get a tax refund. Easy right?

Well, if you earn any income outside of a job that withholds your taxes, such as if you’re a self-employed individual, then you’ll need to pay estimated taxes. You may also need to make estimated tax payments if you’ve received any other non-work income that isn’t subject to income tax withholding, such as capital gains.

You should be making these estimated tax payments each quarter based on your expected adjusted gross income. The idea is that these quarterly estimated payments will be close enough to withholding.

There is one exception though, known as the safe harbor rule.

What Are the Safe Harbor Tax Rules?

The IRS knows that people who aren’t working a traditional W-2 job might have irregular income. So they offer some leeway and won’t punish you if you’re a little short.

The safe harbor provisions are:

- If you expect to owe less than $1,000 after subtracting your income tax withheld, you’re safe.

- If you pay 100% of the previous year’s tax liability via estimated quarterly tax payments, you’re safe. If your adjusted gross income for the year is over $150,000, then it’s 110%.

- If you pay 90% of your current year’s tax liability, you’re safe.

So they expect you to be close (or over), and won’t penalize you if you don’t get it exactly right.

There are also special rules for farmers, fishers, and certain high-income taxpayers. Your state will also have estimated tax payment rules that may differ from the federal rules.

Making Estimated Tax Payments: Due Dates for 2024

The estimated tax payments are due quarterly. And those dates are roughly the same each year: the 15th of April, June, September, and the following January.

From time to time the actual day slides, due to holidays and weekends.

For the 2024 tax year, the dates to pay estimated taxes are:

| Earning Period (Quarter) | Due Date |

|---|---|

| First Quarter (income earned Jan – March) | April 15th, 2024 |

| Second Quarter (income earned April – June) | June 17th, 2024 |

| Third Quarter (income earned July -Sept) | September 16th, 2024 |

| Fourth Quarter (income earned Oct – Dec) | January 15th, 2025* |

* If you file your tax return by January 31st, you do not need to make the fourth quarter estimated payment. You can simply calculate your actual taxes due and pay it with your return.

Calculating Estimated Tax Payments

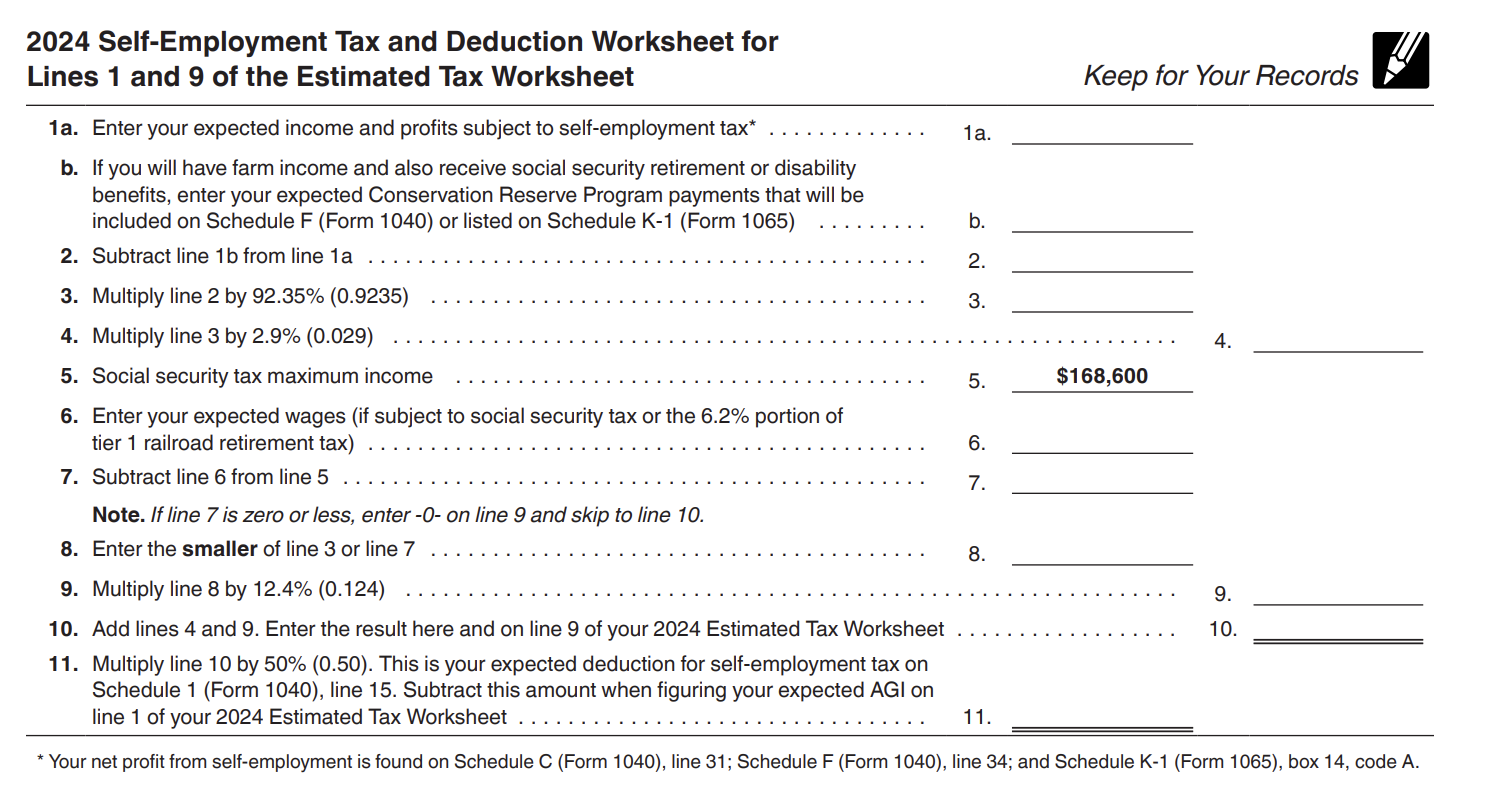

If you have self-employment income, there are two parts to calculating how much you need to pay. The first involves self-employment tax. Self-employment taxes add a wrinkle when calculating what you owe but the IRS can help.

The IRS has a worksheet included in the Form 1040-ES package that you can use to calculate it better based on your expected income:

That same workbook has a tax rate schedule you can use to calculate the taxes you might owe. Use that to figure your estimated payments and you’ll likely be within the 90% safe harbor rule.

Next, you’ll need to check out page 8 of the document for the estimated tax worksheet, which relies on your income and tax bracket to figure out your taxes due:

How to Pay Estimated Taxes to the IRS

If you want to make your payment online, there are several options on the IRS website for paying your taxes. One of the most common is to use the Electronic Federal Tax Payments System to make your estimated payments, but that requires creating another account you will need to manage.

Personally, I just pay via mail because then I have a canceled check as my record. It’s how I’ve done it for years so I never felt a need to change it. You can start by downloading Form 1040-ES and the payment vouchers are on pages 10 and 11.

Where you send your payment depends on where you live, just like where you would mail your tax returns (yo, e-file! you get your tax refund faster!).

| Where You Live | Where To Send |

|---|---|

| Alabama, Arizona, Florida, Georgia, Louisiana, Mississippi, New Mexico, North Carolina, South Carolina, Tennessee, Texas | Internal Revenue Service P.O. Box 1300 Charlotte, NC 28201-1300 |

| Arkansas, Connecticut, Delaware, District of Columbia, Illinois, Indiana, Iowa, Kentucky, Maine, Maryland, Massachusetts, Minnesota, Missouri, New Hampshire, New Jersey, New York, Oklahoma, Rhode Island, Vermont, Virginia, West Virginia, Wisconsin | Internal Revenue Service P.O. Box 931100 Louisville, KY 40293-1100 |

| Alaska, California, Colorado, Hawaii, Idaho, Kansas, Michigan, Montana, Nebraska, Nevada, Ohio, Oregon, North Dakota, Pennsylvania, South Dakota, Utah, Washington, Wyoming | Internal Revenue Service P.O. Box 802502 Cincinnati, OH 45280-2502 |

| A foreign country, American Samoa, or Puerto Rico | Internal Revenue Service P.O. Box 1303 Charlotte, NC 28201-1303 |

| Guam | Department of Revenue and Taxation Government of Guam P.O. Box 23607 GMF, GU 96921 |

| U.S. Virgin Islands | Virgin Islands Bureau of Internal Revenue 6115 Estate Smith Bay, Suite 225 St. Thomas, VI 00802 |

If you need to speak to someone at the IRS, here is how to reach a live person at the IRS.

Can I Make Unequal Payments?

Generally, you should make estimated tax payments in equal amounts, but it’s OK if some are larger than others due to irregular income.

Most people calculate the safe harbor amount, add some wiggle room, divide by four, and pay that amount. It’s easier to calculate that way and it’s just as safe from a tax perspective — just make sure to keep enough aside in case you have a good year and owe more in federal taxes come April.

Also, for the last payment in January, you don’t need to make it if you file your tax return by January 31st.

What If I Fail to Pay?

If you don’t pay enough, the IRS will assess an underpayment penalty. You’ll just owe taxes plus a bit for the penalty.

However, if your failure to pay is due to a disaster or other unusual circumstance or if you retired or became disabled during the tax year of the estimated payments, the underpayment penalty may be waived.

The Bottom Line

If you don’t have taxes taken off your paycheck, your estimated taxes need to be paid quarterly, to avoid penalties come tax time. But, since it’s difficult to guess your total tax liability (especially if you have self-employment or irregular income), the safe harbor rule acts like a safety net.

So long as you pay the previous year’s estimated tax liability or close to the current year’s liabilities, you’ll safely avoid unnecessary penalties.

Other Posts You May Enjoy:

How to File Back Taxes for Free

People fail to file tax returns for different reasons. But if you owe back taxes, it's critical that you file as soon as possible. After all, you can't hide from the IRS forever. Besides, you could be missing out on valuable tax credits or even a big refund. Here's how to file back taxes for free.

How Much Should Tax Preparation Cost in 2024?

Taxes can be scary but it's nothing compared to how much it can cost to have an accountant prepare your taxes! See how much you'll have to pay a professional and a few tips on how you can save money.

States That Don’t Tax Retirement Income

Thinking of moving to a lower-cost state after you retire? All things being equal, you're better off, financially speaking, moving to a state that doesn't tax retirement income. But which states are those and what other factors should you consider? Here is a list of nine states that don't charge income tax. Learn more.

2023 Year End Tax Moves You Must Be Doing

As we near the end of the year, there are a few last minute tax moves you can make to save some money. Not every move on the list will fit your situation, or be right for you, but check it out to find out. It's time to keep more of your money!

Share This Post:

About Jim Wang

Jim Wang is a forty-something father of four who is a frequent contributor to Forbes and Vanguard's Blog. He has also been fortunate to have appeared in the New York Times, Baltimore Sun, Entrepreneur, and Marketplace Money.

Jim has a B.S. in Computer Science and Economics from Carnegie Mellon University, an M.S. in Information Technology - Software Engineering from Carnegie Mellon University, as well as a Masters in Business Administration from Johns Hopkins University. His approach to personal finance is that of an engineer, breaking down complex subjects into bite-sized easily understood concepts that you can use in your daily life.

One of his favorite tools (here's my treasure chest of tools, everything I use) is Empower Personal Dashboard, which enables him to manage his finances in just 15-minutes each month. They also offer financial planning, such as a Retirement Planning Tool that can tell you if you're on track to retire when you want. It's free.

Opinions expressed here are the author's alone, not those of any bank or financial institution. This content has not been reviewed, approved or otherwise endorsed by any of these entities.